Everything You Need to Know About Corporate Fixed Deposits

What is Corporate Fixed Deposits (Corporate FDs)?

Corporate Fixed Deposits are debt instruments issued directly by companies (commonly NBFCs, housing finance companies, or large corporates) to raise funds from the public or selected investors. They function like bank fixed deposits — you lend money to the issuer for a fixed tenure in return for a pre-agreed interest rate — but are issued by corporates instead of banks. Corporate FDs typically offer higher interest rates than bank FDs to compensate for increased credit risk. While they provide predictable cash flows and flexible payout options, they are not covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC) protection that bank deposits enjoy, so the safety of principal and interest depends on the issuer’s credit quality and financial strength.

Advantages of Corporate Fixed Deposits (Corporate FDs)

- Higher interest rates than comparable bank FDs, improving fixed-income yield

- Flexible tenures and payout options (monthly/quarterly/annual/cumulative) to suit income needs

- Useful for diversification of fixed-income portion beyond banks and government securities

- Some issuers offer secured FDs (backed by collateral) which can reduce credit risk

- Simple documentation and nomination facility similar to traditional FDs

How to Choose the Best Corporate Fixed Deposits (Corporate FDs)?

When selecting a Corporate FD, prioritise issuer creditworthiness — check independent credit ratings (CRISIL, ICRA, CARE), recent financial statements, profitability, and leverage ratios. Prefer issuers with stable cash flows, strong promoters, and transparent disclosures. Compare effective yields (annualised rate, compounding frequency), premature withdrawal rules and penalties, tenure alignment with your liquidity needs, and whether the deposit is secured or unsecured. Understand tax treatment (interest is taxable and may attract TDS) and confirm the process for claims/repayment. Avoid over-concentrating in one issuer and consider laddering deposits across maturities and issuers to manage liquidity and reinvestment risk.

Ways to Invest in Corporate Fixed Deposits (Corporate FDs)

Directly via the Issuing Company

Subscribe through the company’s website, investor desk, or branch channels during an open offer — often the simplest route for retail investors.

Through Authorised Distributors / Brokers

Purchase via financial advisors, broker networks, or agent channels that distribute corporate FD offerings and can help with documentation.

Online Marketplaces & NBFC Portals

Use NBFC or aggregator platforms that list corporate deposit offers, enabling easy comparison, online KYC, and payment.

Via Demat/NCD Route (where applicable)

In some cases issuers provide NCDs or dematerialised instruments; buying through demat accounts helps with custody and secondary market visibility if tradable.

Types of Corporate Fixed Deposits (Corporate FDs)

Cumulative Corporate FD

Interest compounds periodically and the entire principal plus accumulated interest is paid at maturity — ideal for growth-focused investors.

Non-Cumulative Corporate FD

Interest is paid out at regular intervals (monthly/quarterly/annual) — suited for retirees or those needing steady income.

Secured vs Unsecured Corporate FD

Secured deposits are backed by specific collateral or charge on assets (lower credit risk), while unsecured deposits rely solely on issuer’s balance sheet (higher risk, often higher yield).

Senior Citizen FD

Many issuers offer special rates or benefits for senior citizens — check eligibility and rate uplift before investing.

Floating-Rate Corporate FD

Interest rate may reset periodically according to a defined benchmark — useful when you expect rates to move and want dynamic yields.

Short-Term / Long-Term Tenures

Tenures typically range from 1 to 5 years (short-term) to longer durations; choose based on liquidity needs and interest-rate outlook.

Grow your wealth with SIP

4,000+ Mutual Funds to choose from

Corporate Fixed Deposits vs Bank Fixed Deposits

Our Associates

Benefits of Investing in Corporate Fixed Deposits with Ideas2Invest

Ideas2Invest offers over 4,000 Mutual Fund schemes without any hidden charges or fees, making your investment journey safer, easier, and more rewarding.

Our advanced tools and calculators offer a simple yet superior investment journey and aid your decision-making.

Whether through SIP (Systematic Investment Plan) or a lump sum, you can invest in Mutual Funds seamlessly on Ideas2Invest with complete ease.

Download our Wealth Magic App from the Play Store or App Store on your device and start your investment journey in just a few minutes.

Trust

We have gained the faith of 500+ happy customers over the two decades, Ideas2Invest has built unmatched trust in the financial services industry.

Expert Support

Get guidance from certified financial advisors whenever you need assistance. Our team of experts is always ready to assist you.

Research Backed Recommendations

Our advisory is backed by top-grade research & data-driven analysis empowering you to make confident financial decisions.

Seamless Investing Experience

Enjoy hassle-free investment processes. From quick account opening to automated SIPs, everything is designed for your convenience.

Who Should Invest in Corporate Fixed Deposits?

Conservative Investors

Individuals who prefer stable, low-risk returns and are not comfortable with equity market volatility.

Retirees & Senior Citizens

Those seeking regular income through higher interest payouts compared to traditional bank FDs.

First-Time Investors

New investors who want a simple and safe starting point before exploring higher-risk investment products.

High Tax Bracket Individuals

Investors who want to balance their portfolio with fixed-income products that offer predictable returns.

Short to Medium-Term Planners

Those looking to park funds safely for 1–5 years with guaranteed returns, better than traditional savings accounts.

How to Invest in How to Invest in Corporate Fixed Deposits? Through Ideas2invest

Choose a Trusted Company

Select a reputed corporate issuer with a strong credit rating (AAA/AA) to minimize default risk.

Complete KYC & Application

Submit your PAN, Aadhaar, bank details, and other documents as required for compliance.

Receive FD Certificate

Obtain the FD receipt or certificate that confirms your investment, tenure, and maturity value.

Check FD Scheme Details

Review the interest rate, tenure options, payout frequency (monthly/quarterly/annual), and premature withdrawal rules.

Make the Investment

Deposit the investment amount via cheque, online transfer, or UPI into the corporate FD scheme.

Enjoy Fixed Returns

Sit back and earn guaranteed interest payouts or a lump sum at maturity as per your chosen plan.

Take Charge of Your Financial Future

Get expert advice and start investing with confidence today.

Get StartedOur Corporate Fixed Deposits Process

Case Study: How Corporate Fixed Deposits Work

See how investors can earn higher fixed returns with Corporate FDs compared to traditional bank deposits

Meet Priya

Priya, a 35-year-old working professional, wants to invest a part of her savings for stable returns, but better than what her bank FD offers.

Initial Investment

She invests ₹5,00,000 in a highly-rated Corporate FD with a tenure of 3 years, offering an annual interest rate of 8.5%.

Growth Opportunity

Compared to her bank FD at 6.5%, the Corporate FD provides significantly higher interest income while still being fixed-return and relatively stable.

Final Outcome

At the end of 3 years, Priya’s investment grows to ₹6,38,000 — giving her ₹88,000 more than what she would have earned in a regular bank FD.

Download Our Mobile Application

Manage your investments on the go, track your portfolio, and stay up to date — all from your phone.

Get the link to download the App.

Frequently Asked Questions

Ideas2Invest is an AMFI Registered Mutual Fund Distributor providing investment advisory, wealth management, and financial planning services.

Yes, our initial consultation is completely free to help you understand your investment options.

You can start by filling out the contact form, and our team will get back to you within 24 hours.

Yes, we provide ELSS and other tax-saving investment solutions.

We offer mutual fund investments, insurance solutions, portfolio management, and more tailored financial services.

Yes, we are AMFI Registered Mutual Fund Distributor with ARN - 113588.

Get in Touch

Latest Insights & Articles

Stay updated with the latest trends in investments and financial planning.

Mutual Funds

Mutual FundsLearn what mutual funds are, how they work, and how to start investing today.

Read More Mutual Funds

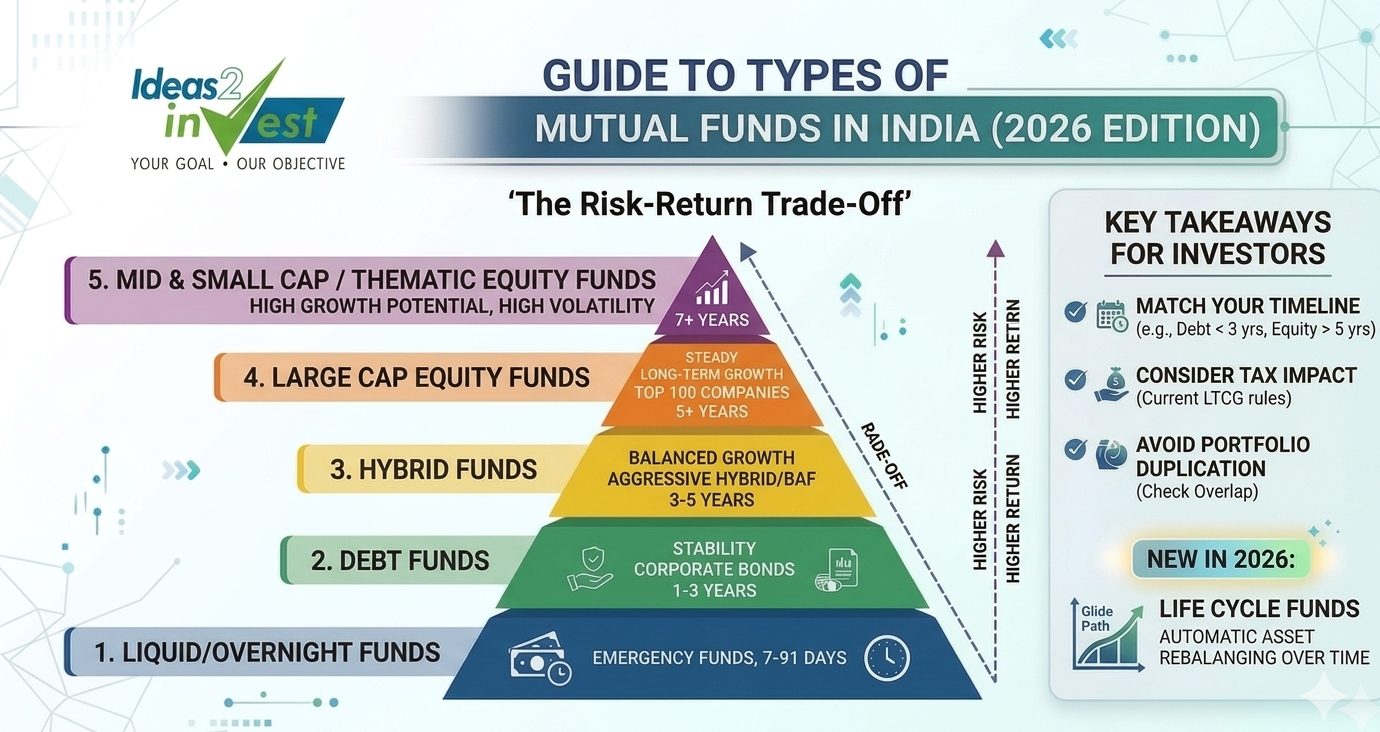

Mutual FundsNavigate the updated 2026 SEBI landscape, from Equity and Debt to the new Life Cycle Funds.

Read More Investment Strategy

Investment StrategyIs your SIP on autopilot? Discover how simple shifts like 'Step-Up' and 'Goal Labeling' can double your wealth.

Read MoreLoading more blogs...