Everything You Need to Know About NRI Taxation in India

What is NRI Taxation & Compliance?

NRI Taxation covers the tax rules, reporting and repatriation norms that apply to Non-Resident Indians (NRIs) who earn or invest in India. Tax liability depends on an individual’s residential status under the Income Tax Act — NRIs are ordinarily taxable only on income that accrues or arises in India. Common taxable heads for NRIs include rental income, capital gains from sale of Indian assets, interest on NRO accounts/FDRs and dividends (subject to specific rules). NRIs must also comply with TDS (Tax Deducted at Source) provisions, claim relief under applicable Double Taxation Avoidance Agreements (DTAAs), and file Indian tax returns when required. Understanding account choice (NRE / NRO / FCNR), repatriation limits, and timely documentation is essential to optimise taxes and ensure regulatory compliance.

Advantages of NRI Taxation & Compliance

- Clear framework under FEMA, RBI & Income Tax law that defines what income is taxable in India

- Repatriation options (NRE/FCNR) that can protect foreign-currency principal and simplify fund flows

- DTAA relief available for many jurisdictions — helps avoid double taxation on the same income

- Wide range of investment options with distinct tax treatment (NRE/FCNR tax-favoured for interest, mutual funds and equities with capital gains rules)

- Digital banking and streamlined KYC make remote tax compliance and filing easier for NRIs

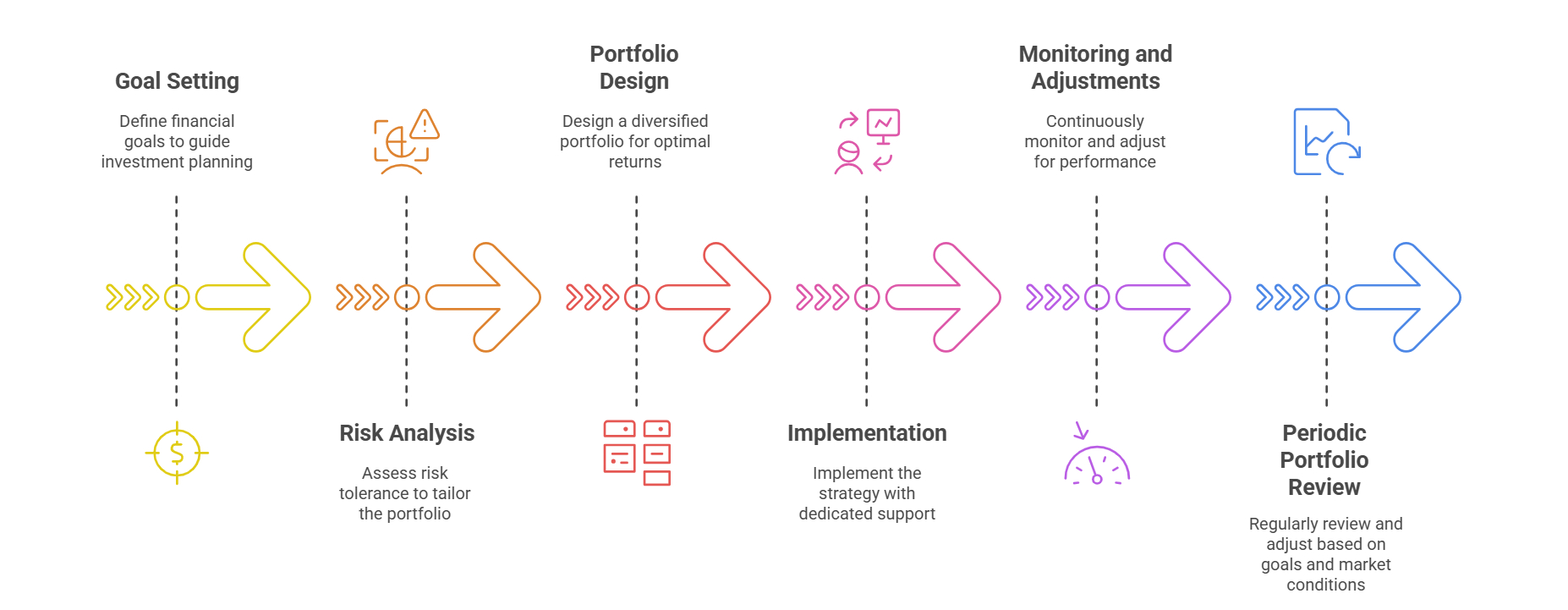

How to Choose the Best NRI Taxation & Compliance?

Start by determining your residential status for tax purposes and list your Indian-source incomes. Choose account types aligned to your goals — use NRE/FCNR for fully repatriable INR/foreign-currency holdings, and NRO for Indian-source income that may require local taxation. Select investment products that match your repatriation needs and tax appetite: for example, NRE FDs/FCNR for tax-efficient deposits, PIS route for direct equities, and mutual funds for diversified exposure. Check DTAA provisions with your country of residence to understand creditability and withholding implications. Finally, engage a cross-border tax advisor or your bank’s NRI desk to structure investments, claim refunds, and prepare accurate ITRs when necessary.

Ways to Invest in NRI Taxation & Compliance

NRE / NRO / FCNR Bank Accounts & Fixed Deposits

Core accounts for NRIs — NRE (INR deposits, fully repatriable, interest generally tax-free), NRO (for Indian income, interest taxable), and FCNR (foreign-currency deposits to avoid forex risk).

Mutual Funds & ETFs

Equity and debt mutual funds are accessible to NRIs (subject to KYC/PIS rules for some flows); pay attention to capital gains taxation and repatriation via bank accounts.

Direct Equity (via Portfolio Investment Scheme - PIS)

Buy listed Indian stocks through the PIS route (RBI-regulated), enabling direct market exposure while complying with reporting and repatriation norms.

Bonds, Corporate Debt & Government Securities

Invest in government securities, corporate bonds or NCDs (subject to eligibility) for predictable income—understand tax treatment and any withholding requirements.

Real Estate, REITs & INVITs

Direct property investment (with certain FEMA restrictions) or listed real-estate vehicles like REITs/INVITs for liquidity and professional management; capital gains and rental income are taxable in India.

Alternatives (PMS, AIFs, Private Equity)

Eligible NRIs (subject to minimums and investor criteria) can access AIFs, PMS or private equity for institutional-style exposure — these carry specific tax and lock-in considerations.

Types of NRI Taxation & Compliance

Tax on Interest & Deposits

Interest from NRO accounts is taxable in India and may attract TDS; interest on NRE/FCNR deposits is typically tax-exempt in India for NRIs.

Capital Gains Tax

Capital gains from listed securities, mutual funds and property are taxed in India — short-term and long-term rates differ and some exemptions/indexation apply for property.

Dividend & Other Income

Dividends, rental income and business income sourced in India are taxable; TDS may be applicable at source with possible DTAA relief.

Withholding & TDS Mechanisms

Many payments to NRIs (interest, dividends, sale proceeds) are subject to TDS; NRIs should track TDS certificates and claim refunds via ITR if over-deducted.

Repatriation Rules

Manage repatriation using NRE/FCNR accounts for free movement of funds; NRO repatriation has prescribed limits and documentation requirements.

DTAA & Foreign Tax Credits

Where India has DTAA with an NRI’s country of residence, the taxpayer can claim tax credits or reduced rates — always preserve documentation and residency proofs to claim benefits.

Grow your wealth with SIP

4,000+ Mutual Funds to choose from

NRI Taxation vs Resident Indian Taxation

Our Associates

Benefits of Investing in NRIs Taxation with Ideas2Invest

Ideas2Invest offers over 4,000 Mutual Fund schemes without any hidden charges or fees, making your investment journey safer, easier, and more rewarding.

Our advanced tools and calculators offer a simple yet superior investment journey and aid your decision-making.

Whether through SIP (Systematic Investment Plan) or a lump sum, you can invest in Mutual Funds seamlessly on Ideas2Invest with complete ease.

Download our Wealth Magic App from the Play Store or App Store on your device and start your investment journey in just a few minutes.

Trust

We have gained the faith of 500+ happy customers over the two decades, Ideas2Invest has built unmatched trust in the financial services industry.

Expert Support

Get guidance from certified financial advisors whenever you need assistance. Our team of experts is always ready to assist you.

Research Backed Recommendations

Our advisory is backed by top-grade research & data-driven analysis empowering you to make confident financial decisions.

Seamless Investing Experience

Enjoy hassle-free investment processes. From quick account opening to automated SIPs, everything is designed for your convenience.

Who Needs to Understand NRI Taxation in India?

NRIs with Rental Income in India

Individuals earning income from properties in India (residential or commercial) must comply with TDS and file ITR to report this income.

NRIs Investing in Mutual Funds & Stocks

NRIs who invest in Indian equities, mutual funds, or bonds are subject to capital gains tax—making proper tax planning crucial.

NRIs with Fixed Deposits & Bank Interest

Interest earned on NRO fixed deposits and savings accounts is fully taxable in India, with TDS applied at source.

NRIs with Global Income but Indian Links

Those with income abroad but financial ties in India need to ensure they are not considered 'Residents' under FEMA or Income Tax rules.

NRIs Seeking DTAA Benefits

NRIs residing in countries with a Double Taxation Avoidance Agreement (DTAA) with India must understand how to claim relief effectively.

How to Invest in How to Manage Your NRI Taxation in India? Through Ideas2invest

Determine Residential Status

Check your residency status under the Income Tax Act (NRI, Resident, or RNOR), as it decides your taxable income in India.

Understand TDS & DTAA

Review how much tax is deducted at source (TDS) and apply Double Taxation Avoidance Agreement (DTAA) benefits, if applicable.

Plan with a Tax Advisor

Work with professional advisors to optimize your tax liability, ensure compliance, and plan future investments tax-efficiently.

Identify Taxable Income Sources

Evaluate income earned in India—such as rent, dividends, capital gains, or FD interest—that is subject to taxation.

File Your Income Tax Return (ITR)

Ensure timely filing of ITR in India if you earn taxable income, claim refunds, or adjust TDS already deducted.

Take Charge of Your Financial Future

Get expert advice and start investing with confidence today.

Get StartedOur NRIs Taxation Process

Case Study: Understanding NRI Taxation in India

See how taxation rules apply differently for NRIs compared to residents

Meet Raj

Raj, an NRI living in Dubai, earns rental income from his apartment in Mumbai and also invests in Indian mutual funds.

Rental Income

Raj earns ₹50,000 per month in rental income. This income is taxable in India, with 30% TDS deducted by the tenant before payment.

Mutual Fund Investment

He invests ₹10 lakh in Indian mutual funds. When redeemed, capital gains tax applies at 20% (long-term) with indexation benefits.

DTAA Relief

Since Raj also files taxes in Dubai (where income is tax-free), he benefits from India-UAE DTAA provisions, avoiding double taxation.

Final Outcome

By filing his Indian ITR and claiming DTAA relief, Raj manages his tax liability effectively, ensuring compliance while optimizing returns.

Download Our Mobile Application

Manage your investments on the go, track your portfolio, and stay up to date — all from your phone.

Get the link to download the App.

Frequently Asked Questions

Ideas2Invest is an AMFI Registered Mutual Fund Distributor providing investment advisory, wealth management, and financial planning services.

Yes, our initial consultation is completely free to help you understand your investment options.

You can start by filling out the contact form, and our team will get back to you within 24 hours.

Yes, we provide ELSS and other tax-saving investment solutions.

We offer mutual fund investments, insurance solutions, portfolio management, and more tailored financial services.

Yes, we are AMFI Registered Mutual Fund Distributor with ARN - 113588.

Get in Touch

Latest Insights & Articles

Stay updated with the latest trends in investments and financial planning.

Mutual Funds

Mutual FundsLearn what mutual funds are, how they work, and how to start investing today.

Read More Mutual Funds

Mutual FundsNavigate the updated 2026 SEBI landscape, from Equity and Debt to the new Life Cycle Funds.

Read More Investment Strategy

Investment StrategyIs your SIP on autopilot? Discover how simple shifts like 'Step-Up' and 'Goal Labeling' can double your wealth.

Read MoreLoading more blogs...